One app for all your study abroad needs

One app for all your study abroad needs

Generally, firms or customers open a current account with a bank, make transactions, and record it, they maintain a bank column in the cashbook. Bank also opens a separate account for each firm or customer in its ledger and supplies a copy of it to the customer. Sometimes, the entries made in both the passbook and cashbook do not match with each other. Therefore, a statement is prepared to identify reasons for the difference in the balance of both the books and also totally the balances called bank reconciliation statements. The same is duly explained in the 5th chapter of class 11 Accountancy, let us go through the topic and analyze it in detail.

This Blog Includes:

- What are Bank Reconciliation Statements?

- Purpose of Bank Reconciliation

- Requirements to Create BRS

- Difference Between Bank Statements and Company’s Accounts

- Bank Reconciliation Statement Example

- Recording of Transactions in Cashbook and Passbook

- Process of Balancing Cashbook and Passbook

- Importance of Bank Reconciliation Statements

- Steps to Prepare Bank Reconciliation Statements

- Bank Reconciliation Statement Format

- Bank Reconciliation Statement Rules

- Bank Reconciliation Statement in Tally

- Bank Reconciliation Statement Class 11 MCQs

- FAQs

What are Bank Reconciliation Statements?

A bank reconciliation statement is a financial statement prepared to reconcile the differences in the balance of the bank column of cashbook and passbook by showing all the causes of difference between the two.

Purpose of Bank Reconciliation

A bank reconciliation is there to compare your records to those of your banks. It checks if there are any two different sets of records for you and the bank in cash transactions. The ending balance of your version will be called the ‘book balance’. The bank’s version for the same is called ‘bank balance’.

Requirements to Create BRS

A bank reconciliation statement needs the use of both the current and prior month’s statements, as well as the account’s closing balance. Because transactions may still be occurring on the actual statement date, the accountant normally creates the bank reconciliation statement utilizing all transactions from the previous day.

Difference Between Bank Statements and Company’s Accounts

When banks deliver a bank statement to a firm that includes the company’s beginning cash balance, transactions throughout the period, and ending cash balance, the bank’s ending cash balance and the company’s finishing cash balance nearly always disagree. The following are some of the causes behind the disparity:

- Deposit Transit: Cash and checks that have been received and recorded by the company but have not yet been recorded on the bank statement.

- Outstanding Checks: Checks that have been issued by the company to creditors but the payments have not yet been processed.

- Bank Service Fees: Banks deduct charges for services they provide to customers but these amounts are usually relatively small.

- Interest Income: Banks pay interest on certain types of bank accounts.

- Not Sufficient Funds (NSF) Checks: When a client deposits a check into an account but the account of the check’s issuer does not have enough money to cover the check, the bank deducts the previously credited check from the customer’s account. The check is subsequently returned to the depositor as non-sufficient funds check.

Important Note: Many businesses now employ specialist accounting software in bank reconciliation to decrease the amount of effort and modifications necessary, as well as to enable real-time updates.

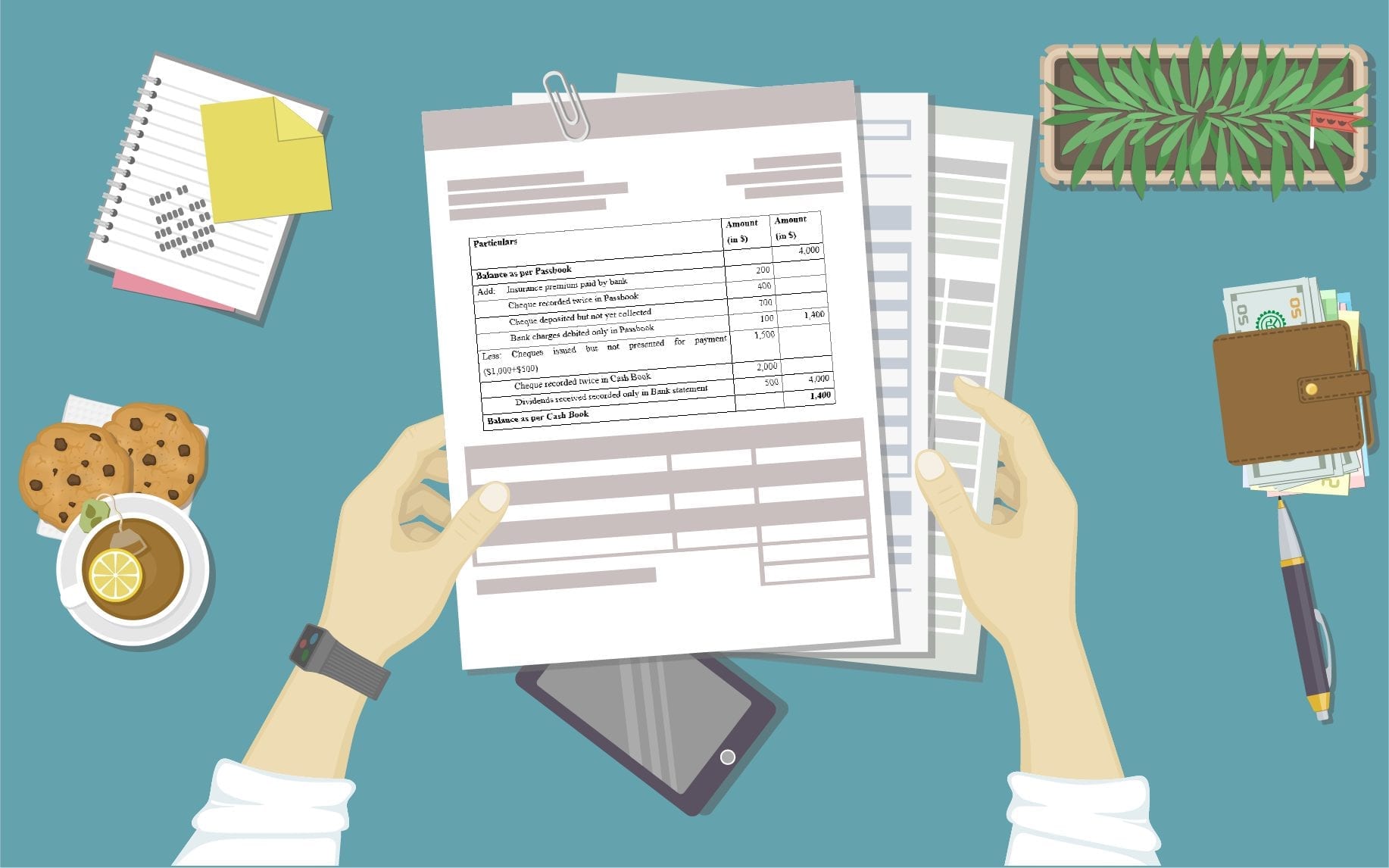

Bank Reconciliation Statement Example

XYZ Company is closing its books and must prepare a bank reconciliation for the following items:

- The bank statement contains an ending balance of INR 300,000 on February 28, 2018, whereas the company’s ledger shows an ending balance of INR 260,900

- The bank statement contains an INR 100 service charge for operating the account

- Bank statement contains interest income of INR 20

- XYZ issued checks of INR 50,000 that have not yet been cleared by the bank

- XYZ deposited INR 20,000 but this did not appear on the bank statement

- A check for the amount of INR 470 issued to the official supplier was misreported in the cash payments journal as INR 370.

- A note receivable of INR 9,800 was collected by the bank.

- A check of INR 520 deposited by the company has been charged back as NSF.

| Amount | Adjustment to Books | |

| Ending Bank Balance | INR 300,000 | |

| Deduct: Uncleared cheques | – INR 50,000 | None |

| Add: Deposit in transit | + INR 20,000 | None |

| Adjusted Bank Balance | INR 270,000 | |

| Ending Book Balance | INR 260,900 | |

| Deduct: Service charge | – INR 100 | Debit expense, credit cash |

| Add: Interest income | + INR 20 | Debit Cash, credit interest income |

| Deduct: Error on check | – INR 100 | Debit expense, credit cash |

| Add: Note receivable | + INR 9,800 | Debit Cash, credit notes receivable |

| Deduct: NSF check | – INR 520 | Debit accounts receivable, credit cash |

| Adjusted Book Balance | INR 270,000 |

Also Read: Commerce Subjects in Class 11 CBSE: Core & Elective

Recording of Transactions in Cashbook and Passbook

When the money is deposited in the bank, firms enter the transaction on the debit side of the bank column of the cashbook, and at the same time, the bank also counts the same transaction on the credit side of the firm’s accounts maintained with it. On the other hand, when the money is withdrawn from the bank, firms enter the transaction on the credit side of the cashbook. At the same time, the bank enters the transaction on the debit side of the firm’s account with it or in the passbook.

Therefore, all the entries recorded on the debit side of the bank column of the cashbook must tally with the entries noted on the credit side of the passbook with the bank. In the same way, all the entries recorded on the credit side of the cashbook must tally with the entries recorded on the debit side of the passbook. Hence, all the entries recorded on the cashbook and passbook must match with each other at any point in time.

Must Refer: Class 11 Applications of Computers in Accounting

Process of Balancing Cashbook and Passbook

One of the most vital distinctions that students of class 11 studying bank reconciliation statements must be through with is that of cashbook and passbook. Both the terms have their significant meaning under this topic. Let us have a look at their differences-

- The cheque is issued to the creditor by the firm and recorded on the credit side of the cashbook. The cheque, however, is presented to the bank after some days. Due to this reason, entries made in the passbook have a time gap with the entry of the cash book

- There is a subsequent time gap throughout the process- such as the day when the firm receives the cheque from the customer, and the firm deposits the cheque to the bank for collection. And, also between the bank making an entry on the debit side of the cash book and recording it on the credit side of the passbook

- When the cheque is received from some other party, it is deposited with the bank, and the entry is made on the cashbook. But, if it is dishonored, then the bank will not make any entry into the passbook

- Sometimes, customers make overdrafts and bank charges interest on it, or there are bank charges and commission charged by the bank from time to time, and the bank debit the firm’s account with it, but the entry in the passbook is made only when the statement is received from the bank

- Banks also collect dividends and interest on customer investment and credit the firm’s account with it or passbook. Still, the customer makes the entry in the cashbook after they receive the statement of the passbook from the bank

Also Read: Highest Salary Jobs for Commerce Students

Importance of Bank Reconciliation Statements

As chapter 5th of class 11 accountancy aims to create a solid foundation for the upcoming topics, it is necessary to understand this one in-depth. Here are some simplified pointers that will help you understand the importance of bank reconciliation statements-

- A bank reconciliation statement shows errors made in both the books by customers or banks and helps to rectify it

- It helps in making future transactions secure with the bank if the customer is sure about the correctness of the balance in the cash book

- It helps in preparing the revised cash book as entries like bank charges, interest allowed or charged by the bank, etc. are recorded in the passbook and will be recorded in the cashbook in the future

- Any fraud made by the bank or any other party can be disclosed through it. For Example: If any staff shows any type of deposit in the bank but is not deposited, then it can be disclosed easily with the help of this statement

- According to the chapter, it helps in keeping track of cheques sent to the bank for collection and reveals the delay in the collection of cheques by the bank

Must Read: Stock Trading Courses

Steps to Prepare Bank Reconciliation Statements

A bank reconciliation statement is prepared when customers or firms get their passbooks updated from the bank. The customers or firms then tally the entries and balance of both cashbook and passbook. Following steps are required to prepare the bank reconciliation statements:

Step 1

Tick the items on the debit side of the cashbook which tally with the items on the credit side of the passbook, and note down the unticked items, which is the cause of the difference in balances of both the books

Step 2

In the same way, tick the items on the credit side of the cash book, which tally with the items on the debit side of the passbook, and note down the unticked items which do not tally in both the books, which is the cause of the difference

Step 3

Now a bank reconciliation statement can be prepared by taking the balance as per the cash book as a starting point. If the statement is started with the bank column of the cashbook, then the answer arrived will be the balance as per the passbook. Then, you can add the items which have the effect of higher balance in the passbook and deduct the items which influence lower balance in the passbook.

Bank Reconciliation Statement Format

Below we have mentioned the Format for Bank Reconciliation Statement:

Credits: Accounting for Management

Now that you are through with the process and steps of bank reconciliation statements, let us go through the pointers which elaborate the entries which can be made in the cashbook or passbook.

Also Read: How to become a Chartered Accountant?

Balance as Per Cashbook can either be Credit or Debit

- Class 11 accountancy chapter bank reconciliation statements mention that the Credit balance as per cash book shows the amount which has been withdrawn more than deposit and credit balance as per cash book is also known as ‘overdraft balance as per cash book’

- Debit balance as per cash book shows that the firm or customer has so much balance of deposit in the bank

Balance as Per Passbook can be either Credit or Debit

- Credit balance as per passbook shows that the firm or customer has a given amount in balance of deposit in the bank

- Debit balance as per passbook shows the amount which has been withdrawn more than the deposit and debits balance as per passbook is also known as ‘overdraft balance as per passbook’

Bank Reconciliation Statement Rules

Rules help in avoiding any mistake in the statement. These rules act as a basic framework for the statement. Here are some of the bank reconciliation statement rules:

- Any debit balance in the cash book is referred to as the deposits of the business entity

- Debit in cash book is equal to credit in passbook

- Credit balance in cash book means unfavorable balance

- Debit balance in cash book means favorable balance

- Cheques that are issued but in any case not presented are adjusted in the cash book

Bank Reconciliation Statement in Tally

Credits: Suman Education Hub

Bank Reconciliation Statement Class 11 MCQs

Mentioned below are the Bank Reconciliation Statement Class 11 MCQs:

1. When a check is not paid by the bank, it is called?

A. Honored

B. Endorsed

C. Dishonored

D. a & b

2. A bank reconciliation statement is prepared by?

A. banker

B. Accountant of the business

C. Auditors

D. Registrar

3. Bank reconciliation is not a_______?

A. Reconcile records

B. Memorandum statement

C. Ledger account

D. Procedure to provide cash book adjustments

4. The balance on the debit side of the bank column of cash book indicates?

A. The total amount has drawn from the bank

B. Cash at the bank

C. The total amount overdraft in the bank

D. None of above

5. Bank reconciliation statement is_______?

A. Part of bank statement

B. Part of the cash book

C. A separate statement

D. A sub-division of journal

6. Uncollected checks are also known as_______?

A. Outstanding checks

B. Uncleared checks

C. Outstation checks

D. Both b & c

7. Unfavorable balance means?

A. Credit balance in the cash book

B. Credit balance in Bank statement

C. Debit balance in the cash book

D. Debit balance in the petty cash book

8. Farkhanda Jabeen Ltd. receives a check for Rs. 100 records it in the cash book and deposits it on the same day. A statement sent by the bank that day does not show this Rs. 100. How is this shown on the bank reconciliation statement?

A. As an uncredited deposit added to the bank statement balance

B. As an uncredited deposit deducted from the bank statement balance

C. As an unprecedented check added to the bank statement balance

D. As an unprecedented check deducted from the bank statement balance

9. Which of the following items is not a reason for the difference between bank balance as per cash book and passbook?

A. Dishonored check

B. Cheques deposited but not yet cleared

C. Credit sales

D. Cheques issued but not yet presented for payment

10. A check that bears a date later than the date of issue is called?

A. Anti dated check

B. Post-dated check

C. Dishonored check

D. Outdated check

Answers

- C

- B

- C

- B

- C

- D

- A

- A

- C

- B

Refer These: (Bank Reconciliation Statement PDFDownload) (Bank Reconciliation Statement Class 11Download)

FAQs

A bank reconciliation statement is prepared by business organizations.

A bank reconciliation statement is a financial statement prepared to reconcile the differences in the balance of the bank column of cashbook and passbook by showing all the causes of difference between the two.

A bank reconciliation statement compares a bank statement with the balance of the company’s accounts with the balance in the bank statement.

Hence, we have presented everything that you must know about the Bank reconciliation statements theory. If you need guidance with career-related queries, then get in touch with the experts of Leverage Edu. Get your free career counselling session through an e-meeting with the team to soar high in your career.

-

Please i need a detail definition of the Dishonored cheque, uncredited and bounced cheque with good examples. thanks

-

Hi, ISAAC!

Thanks for the suggestion. We will surely update you with an article on this!

For more information, reach us at 1800 57 2000!

-

-

excellent

-

Thank you! Hope that you found it helpful.

-

45,000+ students realised their study abroad dream with us. Take the first step today.

45,000+ students realised their study abroad dream with us. Take the first step today.

7 comments

Please i need a detail definition of the Dishonored cheque, uncredited and bounced cheque with good examples. thanks

Hi, ISAAC!

Thanks for the suggestion. We will surely update you with an article on this!

For more information, reach us at 1800 57 2000!

excellent

Thank you! Hope that you found it helpful.

Its helpful for both Teachers and students

We are glad you found it informative.

Glad that you found it helpful.